Solutions / Lacima Analytics / Contracts & Structures

Advanced Models

Apply powerful modelling techniques to capture complex market behaviour.

Your Advanced Modelling Questions

How can I model renewables, weather-driven assets, and complex price behaviours without relying on highly calibrated stochastic models?

Is it possible to reduce model complexity and calibration time while maintaining statistical rigour?

How can I generate realistic Monte Carlo simulations directly from historical behaviour rather than theoretical assumptions?

How do I maintain correlations across multiple risk factors so portfolio simulations remain coherent and realistic?

How can I represent price spikes and non-linear dynamics that standard diffusion models struggle to capture?

How do I combine advanced modelling techniques into a single framework that feeds portfolio valuation and risk reporting?

The Advanced Models module extends Lacima Analytics’ ‘Core’ modelling framework with a suite of specialised techniques designed to model complex assets, price behaviours, and risk relationships that extend beyond standard approaches.

Our Advanced Modelling Solution

Advanced Models provides a flexible modelling toolkit that allows users to tailor model structures to the behaviours observed in real markets.

The module includes a combination of regression-based models, non-linear transformations, specialised spike and hybrid price models, temperature-load relationships, and historically driven simulation techniques, all of which can be applied individually or in combination.

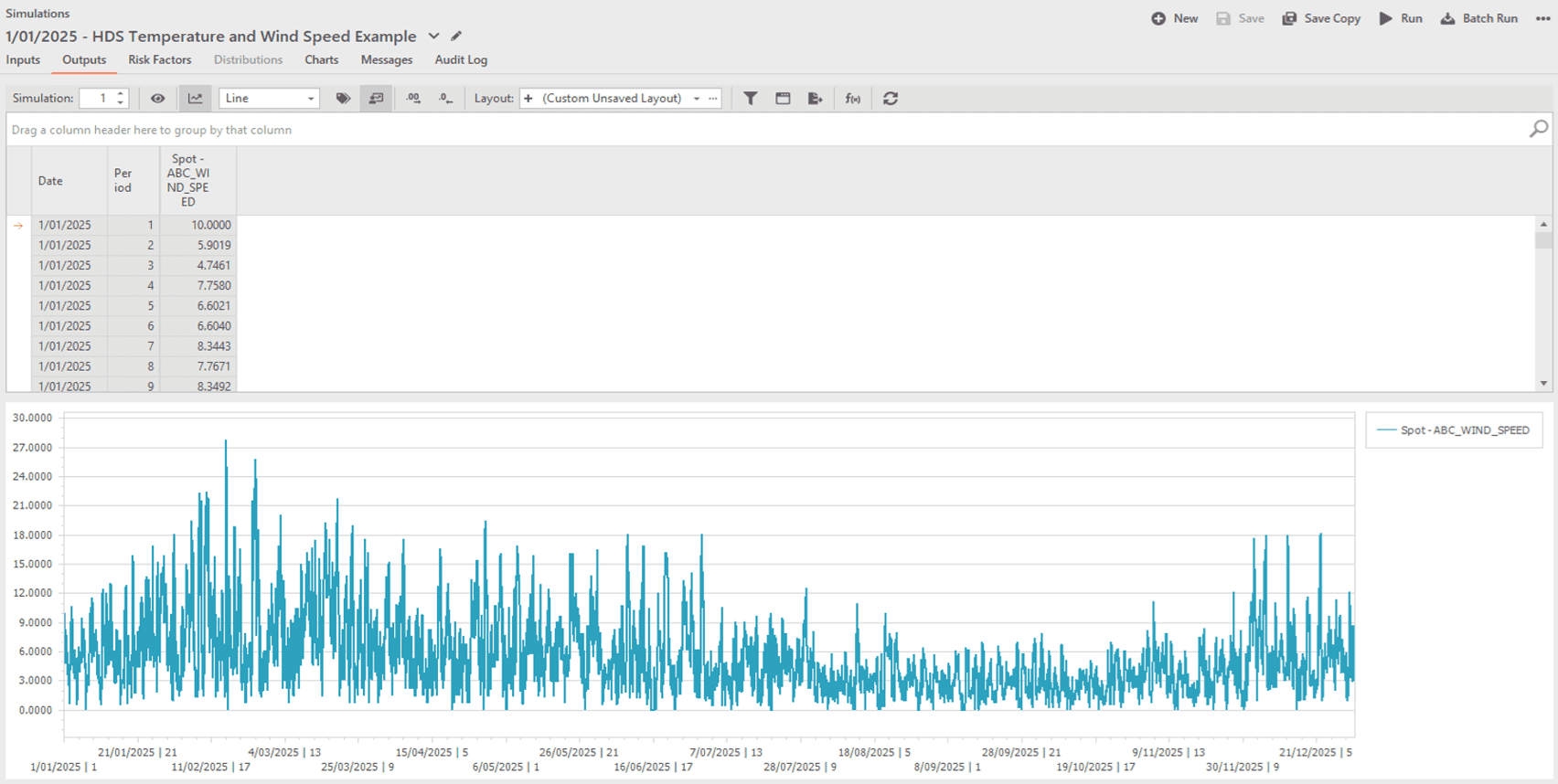

Historical Data Simulation is one of these capabilities, offering a data-driven Monte Carlo approach that generates simulations directly from historical observations. By drawing on observed market behaviour, Historical Data Simulation provides an intuitive alternative for modelling variables such as renewables output, environmental drivers and other complex risk factors without the need for complex calibration of theoretical models.

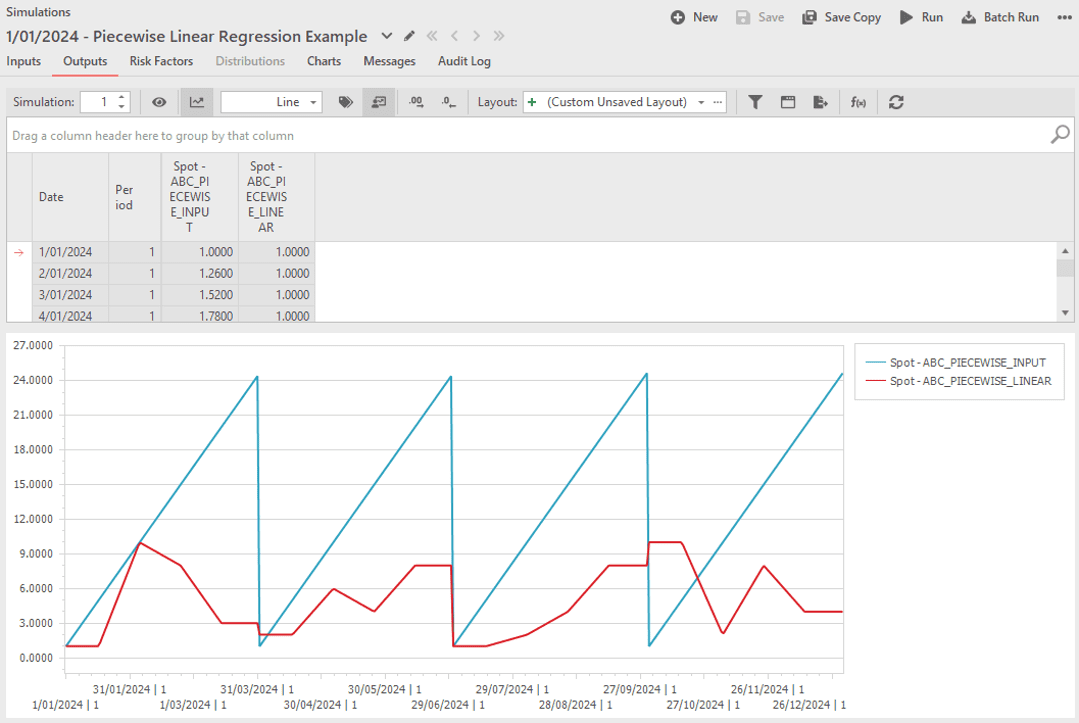

Users can also apply multi-variate and piecewise regression techniques to estimate structured relationships from historical data, model non-linear responses using piecewise transformations, and represent demand dynamics through temperature-load models.

For markets exhibiting extreme behaviour, specialised price spike and hybrid Double Mean Adjustment frameworks extend standard mean-reversion approaches to better reflect observed price dynamics.

All advanced models integrate seamlessly with Lacima Analytics’ simulation, valuation and portfolio analytics framework, ensuring outputs feed directly into P&L, Value-at-Risk, Earnings-at-Risk and Potential Future Exposure calculations.

Model complex, non-linear market relationships using intuitive

piecewise transformations grounded in observed behaviour.

The Advanced Modelling Features

Intuitive visual outputs bring simulated market dynamics to life,

providing actionable insight for faster, more informed decisions.

- Historical Data Simulation

Generate Monte Carlo simulations directly from historical data to capture real-world dynamics without complex calibration. - Piecewise Transformations

Define flexible, time-varying non-linear relationships between inputs and outputs using user-controlled segmentation. - Correlated Multi-Factor Simulations

Preserve cross-factor relationships by simulating multiple risk drivers within a consistent modelling framework. - Advanced Regression Techniques

Apply piecewise linear and multi-variate regressions to model complex relationships between market drivers. - Temperature-Load Modelling

Estimate and simulate demand relationships driven by ambient air temperature at user-defined levels of granularity. - Price Spike & Hybrid Modelling

Capture extreme price behaviour using specialised spike regimes and Double Mean Adjustment. - IFERC Risk Factor Simulation

Generate simulated spot and forward prices that replicate IFERC publication frequency and settlement behaviour for gas markets. - External Simulation Import

Import externally generated spot and forward simulations directly into Lacima’s portfolio analytics. - Forward Curve & Mean Adjustment Integration

Align advanced model outputs with forward curves using configurable mean adjustment controls.

Related Solutions

Lacima Analytics > Core

Advanced Models extends Lacima Analytics Core, enabling more sophisticated modelling within a consistent, enterprise-grade analytics framework.

Lacima Analytics > Valuation (MtM)

Generate accurate Mark-to-Market valuations for complex energy and commodity instruments.

Lacima Analytics > VaR

Use advanced modelling techniques to generate realistic simulations for Value-at-Risk analysis.

Lacima Analytics > EaR

Apply advanced simulations to analyse cashflow uncertainty and Earnings-at-Risk.