Solutions / Lacima Trader

Simulation

Generate fast and accurate Monte Carlo simulations of spot and forward variables.

Your Simulation Questions

Can I avoid the time and resources required to build in-house simulation and calibration engines?

How can I simulate different asset types with a range of different models (Black, single factor, multi factor, spreads etc)?

How can I accurately model historical characteristics in prices and other non-price variables?

How can I model prices and forward curves simultaneously and accurately?

Can I simulate multiple variables in a single model?

How do I ensure my models handle the varied needs of energy and commodity markets?

Our Solution: Simulation

A powerful, flexible Monte Carlo simulation engine that allows the analysis of multiple variables at once. Perform analysis directly using the templates provided or use in conjunction with your existing valuation and risk analysis solutions.

Lacima Trader > Simulation’s flexible, multi-variable design allows simulation of almost any variable, ensuring it can accommodate your unique analysis needs:

- Value and structure a deal

- Identify specific paths of deal value

- Tailor-make risk-reward profiles by combining deals with hedging instruments

- Assess how value moves through time

- Look at deal value extremes to assess ‘at-risk’ components

- Determine the distributions of cash flow and other financial metrics

Developed by the leaders in energy and commodity risk analytics, Lacima’s Monte Carlo engine has helped inform the deal analysis and structuring of some of the largest energy and commodity companies in the world.

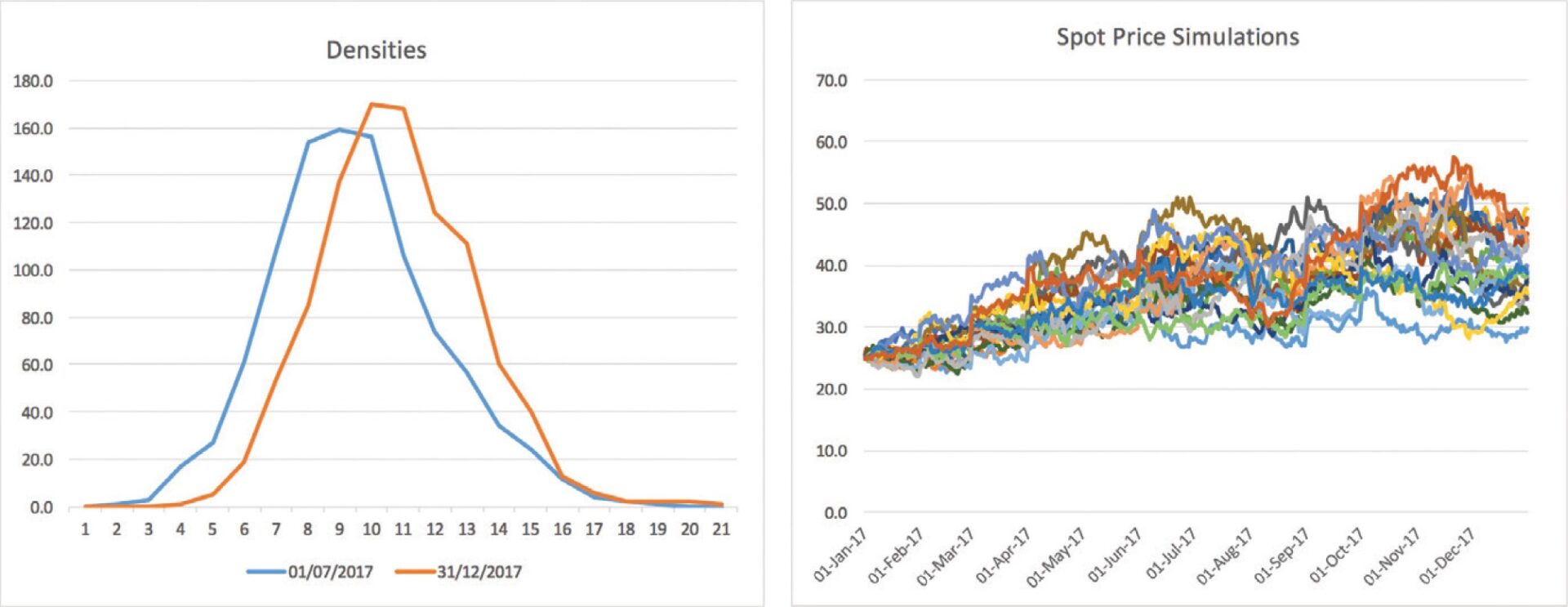

Simulation set-up and sample outputs

Features: Simulation

Spot price densities and simulations

- Generate market simulations and use them to produce Monte Carlo-based deal valuations

- Full range of industry-leading models including single factor jump diffusion, multi factor, user-defined spread, and non-linear models available

- Capture all commodity market behaviours including jumps, mean reversion, seasonality, negative prices, changes in curve shape and structural relationships between prices, volatility, and maturities

- Model calibration ensures an accurate reflection of historical market behaviour

- Output individual spot and forward simulations at various levels of granularity

- Calculate the mean, moments, percentiles, and densities of a set of simulations

- Meets the needs of Front and Middle Office including traders, quants, analysts, and risk managers

- Analyse, view, and graph simulations for detailed analysis

- Customise using Microsoft Excel, VBA, and other Excel add-ins

- Perform analysis directly within Excel or output simulations for use in other models or software

- Same-day implementation and easy to learn with familiar Excel interface

Related Solutions

Curve

Convert forward quotes into detailed arbitrage-free curves. Supports multiple levels of granularity including monthly, weekly, daily, hourly, and half-hourly.

Pricer

Produce and analyse positions, calculate values and risk sensitivities for a wide range of energy and commodity derivative instruments quickly and flexibly.

Storage

Structure, value and hedge gas storage assets and identify the trades required to rebalance a storage portfolio to maximise profit.

Swing

Structure, value, hedge and analyse swing contracts to deliver maximum profits. Utilise indexation and output analysis to understand value drivers.